Andy Grove, founder of Intel said in a meeting with Clayton Christensen:

Disruptive threats come inherently not from new technology but from new business models.

He also defined an Inflection Point as:

A time in the life of a business in which its fundamentals are about to change.

Just think about the following business model disrupters from the past decade:

Craigslist (Pew Research, 2008: more people read news online than paid newspaper subscribers)

Napster

Google Books

Uber

Driverless cars

Defining Business Model

Ed and Ron discussed the book by Alexander Osterwalder and Yves Pigneur, Business Model Generation, wherein they define business model as:

A Business model describes the rationale of how an organization creates, delivers, and captures value.

Notice that a business model deals with capturing value, which is the company’s pricing strategy.

canvas1

When you see a business model, you will probably see a pricing change (from CDs to iTunes .99¢, from Blockbuster video rental to Netflix, etc.).

In the book, the authors explore nine building blocks of the business model:

Customers segments

Value Proposition

Channels

Customer relationships

Revenue streams—customer is heart, RS are its arteries (RM, Dynamic pricing, etc.)

Key resources

Key Activities

Key partnerships

Cost structure

You can find more information about the book, and accompanying App, here.

Disruption Comes from the Outside, and Non-Experts

The daunting task for many companies is:

How to implement and manage new models while maintaining existing ones.

Harvard business professor Clayton Christensen wrote:

Generally, the leading practitioners of the old older become the victims of disruption, not the initiators of it.

Steve Ballmer, former CEO of Microsoft once said:

Google is not a real company. It’s a house of cards.

Michael Dell, when asked what Steve Jobs should do with Apple when he returned in 1987, said:

He should just shutter its doors.

Experts rarely innovate. G.K. Chesterton wrote:

The argument of the expert, that the man who is trained should be the man who is trusted, would be absolutely unanswerable if it were really true that the man who studied a thing and practiced it every day went on seeing more and more of its significance. But he does not. He goes on seeing less and less of its significance.

Consider this, from the book, The Experts Speak: The Definitive Compendium of Authoritative Misinformation (1998):

1986 Gottlieb Daimler predicted auto market would never exceed 1Million because you couldn’t train that many chauffeurs

Robert Milikan, Nobel Prize, phyics, 1920: “There’s no likelihood man can ever tap the power of the atom.”

“We don’t like their sound. Groups of guitars are on the way out.” Decca Records, turning down The Beatles a second time, 1962

Kodak engineer Steve Sasson invented “filmless photography” in 1975, but Kodak’s business model wasn’t designed to deal with any thing but film.

Xerox’s PARC Labs Xerox invented the interface on computers, but Xerox couldn’t figure out how you put a meter on a computer. It just didn’t fit with their business model. Steve Jobs had a different business model idea.

Creativity is Always a Surprise

In The Black Swan, Nassim Nicholas Taleb wrote:

We do not know what we will know. Invention and creativity is always a surprise. If we could prophesy the invention of the wheel, we’d already know what a wheel looks like, and thus we could invent it.

Friedrich Hayek wrote:

The mind can’t see its own advance.

Another book Ron likes on this topic is Seizing the White Space by Mark W. Johnson (2010).

The white space is not uncharted territory or an underserved market, but rather a range of potential activities not defined or addressed by the company’s current business model. It requires a different model to exploit.

Johnson points out that more than 30% of the 350 Business Model Innovations he studied in the past ten years were enabled by internet technology. So it’s not just about technology, but rather a fundamental change in creating and capturing value.

Peter Drucker on Business Models

One of Peter Drucker’s (1909–2005) many articles published in the Harvard Business Review (September-October 1994) was entitled “The Theory of the Business,” which laid out what he considered to be the essential elements executives would have to define in order to create wealth:

Not in a very long time—not, perhaps, since the late 1940s or early 1950s—have there been as many new major management techniques as there are today: downsizing, outsourcing, total quality management, economic value analysis, benchmarking, reengineering. Each is a powerful tool. But, with the exceptions of outsourcing and reengineering, these tools are designed primarily to do differently what is already being done. They are “how to do” tools.

Yet “what to do” is increasingly becoming the central challenge facing managements, especially those of big companies that have enjoyed long-term success.

What accounts for this apparent paradox? The assumptions on which the organization has been built and is being run no longer fit reality. These are the assumptions that shape any organization’s behavior, dictate its decisions about what to do and what not to do, and define what the organization considers meaningful results. These assumptions are about markets. They are about identifying customers and competitors, their values and behavior. They are about technology and its dynamics, about a company’s strengths and weaknesses. These assumptions are about what a company gets paid for. They are what I call a company’s theory of the business.

In fact, what underlies the current malaise of so many large and successful organizations worldwide is that their theory of the business no longer works.

It usually takes years of hard work, thinking, and experimenting to reach a clear, consistent, and valid theory of the business. Yet to be successful, every organization must work one out.

What are the specifications of a valid theory of the business? There are four:

The assumptions about environment, mission, and core competencies must fit reality.The assumptions in all three areas have to fit one another.The theory of the business must be known and understood throughout the organization.The theory of the business has to be tested constantly. It is not graven on tablets of stone. It is a hypothesis. And so, built into the theory of the business must be the ability to change itself.

Even if a particular business did not follow Drucker’s sage advice and postulate a theory of its business, one could certainly argue that since the macroeconomic environment of nearly any developed country is comprised of millions of businesses, the aggregate marketplace is a testable hypothesis in its own right, whereby customers spending their own.

George Gilder on Innovation

In his book, Wealth and Poverty: A New Edition for the Twenty-First Century, George Gilder weighs in on business models and event the efficiency vs. effectiveness debate:

Firms at the top of their S-curves of growth: the time when innovation dwindles and heavily bureaucratized companies seek minor new adaptations, packaging changes, and manufacturing efficiencies in order to wring the last gains of productivity from an essentially static industry that has already long passed its phase of ‘fast history.’

Auto companies at the very pinnacle of productivity had lost all room to maneuver. New developments almost never emerge from the leading companies in an industry. None of the carriage makers and buggy whip producers could create a salable automobile, and the gaslight and candle businesses neglected the promise of electricity; slide rule people at Keuffel and Esser succumbed without response to the handheld calculator; just as IBM lagged behind other companies in adopting most major innovations in business machines, from copiers to word processors; and as even Texas Instruments finally became relatively rigid and uncreative in the microprocessor field.

The very process of rationalization and bureaucracy by which a company becomes the most productive in an industry tends to render it less flexible and inventive. An exclusive preoccupation with statistical productivity—simple coefficients between inputs and outputs—can lead to a rigid, and in the long run, unproductive economy.

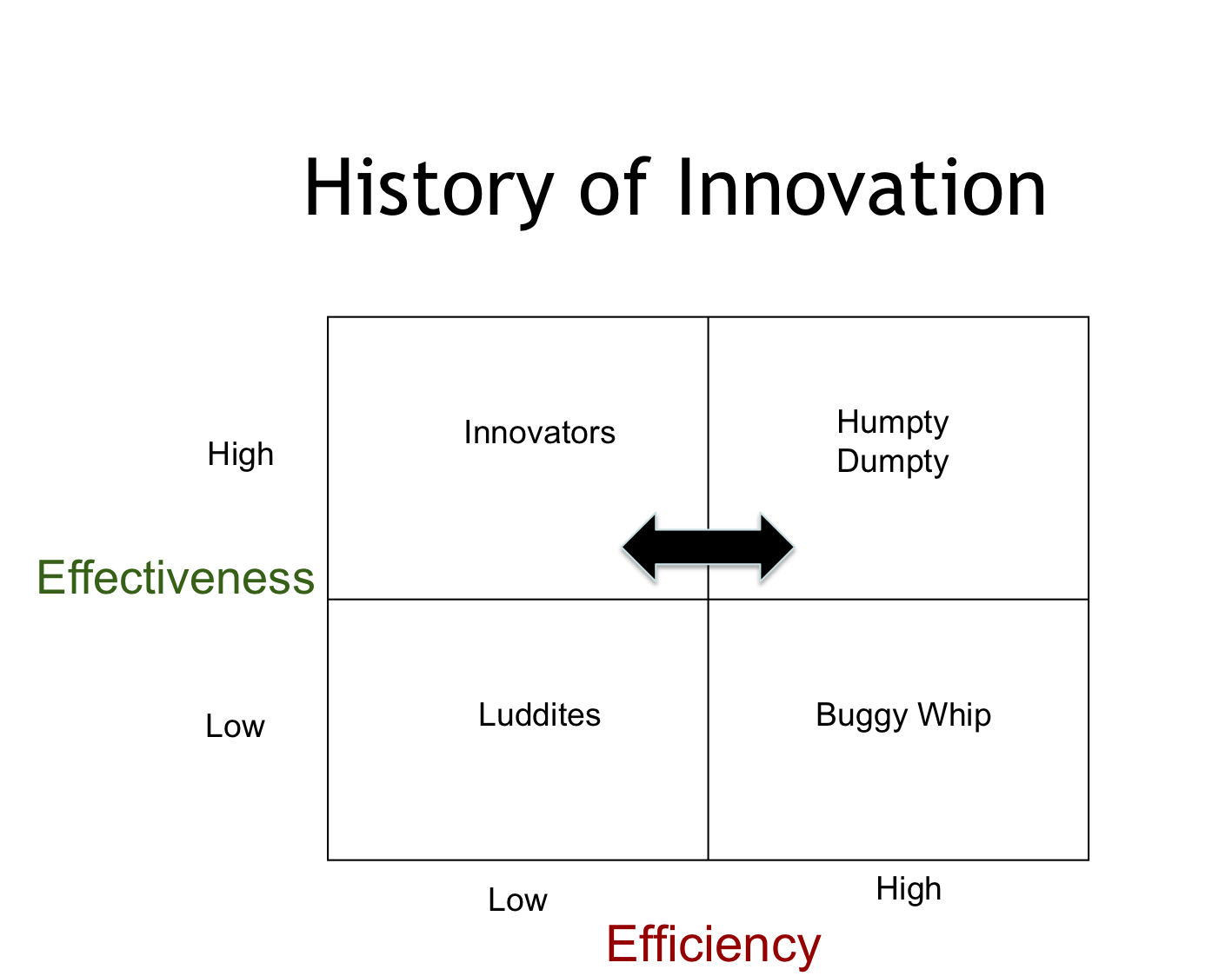

Here's a matrix that explains this phenomenon, from Ron’s book, Implementing Value Pricing: A Radical Business Model for Professional Firms:

History of Innovation

Luddites: Firms that resist technological advances and other innovations that are merely table stakes risk being Luddites. They have both low efficiency in doing things right, and low effectiveness at doing the right things—not a bright future. Fortunately, not many firms are in this category. If you are here, you are dead already and the funeral is a mere detail.

Buggy Whips: Usually when an industry is at the apogee of its efficiency, it is at risk of being made obsolete by new technologies or business models. As Peter Drucker said, no amount of efficiency gains would have saved the buggy whip manufacturers from the automobile.

Innovators: As George Gilder wrote in Forbes, “Knowledge is about the past; entrepreneurship is about the future. If creativity was not unexpected, governments could plan it and socialism would work. But creativity is intrinsically surprising and the source of all real profit and growth” (“The Coming Creativity Boom,” November 10, 2008). Innovators are firms that are willing to invest some of today’s profits into tomorrow, while at the same time sacrificing efficiency for effectiveness. Innovation, creativity, and Total Quality Service are the antithesis of efficiency—ideas such as Google Time, experimenting with new ideas, investing in education, all reduce efficiency metrics. But if firms do not make these essential investments they are simply coasting on their existing intellectual capital, and in today’s economy, knowledge becomes obsolete more rapidly.

Humpty Dumpty: This is a precarious future. This represents firms that are highly efficient and effective. I am arguing if you are here, you better be sliding back to the Innovators position and start sacrificing some of that efficiency for innovation and making the firm more valuable to its customers. Humpty Dumpty eventually falls and ends up like the industries mentioned under Buggy whips. Efficiency is not the answer. Effectiveness is. This is precisely why we warn companies to avoid putting efficiency ahead of effectiveness. Any industry at the apogee of efficiency is an industry in decline.

Parting Thoughts

Embracing a new business model requires leadership and vision. It requires knowing you are doing the right things, not just doing things right. It requires focusing the firm on the external value it creates for the customer and simultaneously building the type of firm people are proud to be a part of and contribute to—the sort of organization you would want your son or daughter to work for. It requires a sense of dignity and self-respect that you are worth every penny you charge, and you will only work with customers who have integrity, whom you enjoy, and respect. It requires an attitude of experimentation, not simply doing things because that is the way it has always been done. It requires less measurement, less fear, and more trust. It requires boldness and risk-taking—there has yet to be a book written titled Great Moderates in History.